Market Letter February 2018

“The market will go up and it will go down, but not necessarily in that order.”

J.P. Morgan

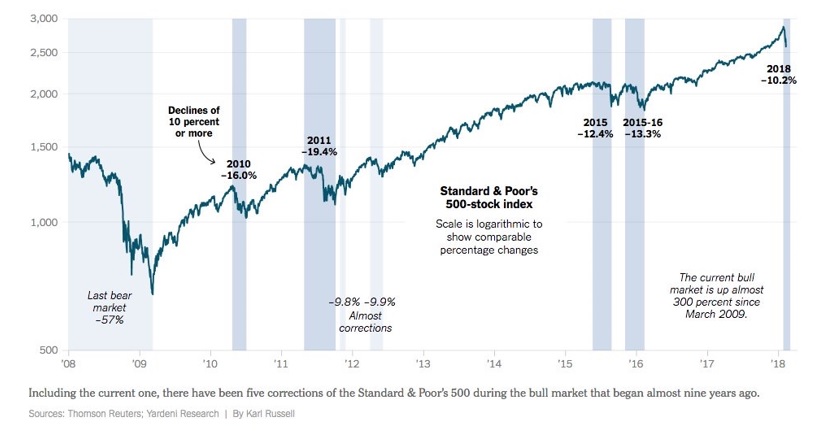

Buckle your seatbelts, volatility is back. After the most placid year since 1964 (source: Bespoke Investment Group), 2018 has started off with an ugly surprise: two 4%+ single-day declines on the Dow Jones Industrial Average that have pushed the index into official “correction” territory (defined as a loss of 10%) for the first time since late 2015. So, what’s going on? As with most market selloffs, there’s never one singular root cause but there are a couple of catalysts. We’ll keep this explanation as short as we can.

First and most importantly, economic data and corporate earnings, the things that really matter to us and should matter to all investors, are healthy and strong. We’re finishing up one of the best quarters for earnings in years and analysts anticipate the April quarter to be even better with revenues increasing by 7%+ and earnings by 14%+ (source: Raymond James’s Equity Strategy Group). We are not concerned that this correction (at this point) is an indicator of a longer-term bear market or the dreaded “r” word: recession.

That being said, we saw the first indications of wage inflation in last Friday’s jobs report. While rising wages means more dollars in peoples’ pockets in nominal terms, it also means a decline in the purchasing power of those dollars in real terms and it means companies must pay their employees more (thus earning less profit). This is overly simplistic, but the key takeaway is that market participants must now recalibrate their expectations to include rising inflationary pressure (which is not necessarily a bad thing in moderation). This will no doubt take some time.

In relation to this, interest rates rose sharply last Friday on the back of another great jobs report and news of US Treasury bond issuance. As interest rates rise, investors can begin to exchange their riskier stocks for safer bonds that now pay better rates of interest. This leads to declines in stocks as well as lower values for bonds with lower coupon payments. To be sure, interest rates on US Treasuries are still extremely low (less than 3% for a 10-year bond and just over 3% for a 30 year bond), and it’s the Federal Reserve’s job to keep them moving higher at a very steady pace towards normal long-term levels.

But certainly a move in interest rates and/or some inflationary pressure is not enough to cause the Dow Jones index to drop nearly 10% in a week. No, the real cause for the sharp decline has been (surprise surprise) complex derivative investment products. In this case, it was a group of vehicles designed to track the opposite movement of the stock market’s Volatility Index (or VIX). You read that correctly: when volatility goes up these “inverse” funds actually decline, and on Monday they started to collapse. Several have now evaporated entirely. The good news is that this type of fund will likely exist no more, but the bad news is that, yet again, investors fail to see the danger in complex investments they don’t understand yet want to own.

Where do we go from here? We wouldn’t be surprised to see this choppy action continue in the short term as additional “inverse volatility funds” dry up (that means more 4% down days are possible). Longer-term, we expect rising rates and the question of inflation to keep market participants on edge. Hopefully, a strong earnings quarter in April and continued positive economic data throughout the rest of 2018 will offer some support to stock prices.

The bigger question is whether this type of volatility is the “new normal.” We think not, but it’s important to remember that some volatility IS normal and that 2017 was decidedly abnormal. In his morning report on 2/9/18, Raymond James’s Jeff Saut reminds us that “the S&P 500 has experienced a 10% correction about every 25 months, on average, going back to 1932.” Furthermore, we included a chart in our August 2017 newsletter which showed that 2.5%+ single-day drops occur, on average, at least several times every year. Up until last Friday, we hadn’t seen even one 2.5% drop since “Brexit” in summer of 2016.

In sum, enduring corrections and panics is a necessary component of being a long-term investor, and it’s why we feel it’s so important for everybody to identify their “pain threshold.” This recent event, being entirely normal but startling after such a calm 2017, represents the ideal opportunity to rethink your risk tolerance. If this type of market action makes you a bit uncomfortable but you have still been able to sleep normally, you’re probably invested appropriately. As always, please don’t hesitate to reach out with questions or to discuss with us this further.

All the best,

Peter & Ben